1) Dollar Strength & Equity Strength. Probability: 1%

2) Dollar Weakness & Equity Strength. Probability: 13%

3) Dollar Weakness & Equity Weakness. Probability: 16%

4) Dollar Strength & Equity Weakness. Probability: 70%

Picking the correct number will be key to determining whether you make or loose money over the next six months. Below I give a brief summary of why I have assigned the respective probabilities. As you’ll see, whichever way you slice it, my outlook is grim, but a stronger dollar and weaker equities is my pick.

1) Dollar Strength & Equity Strength. We are currently in the early stages of a depression. This is just a plain fact. What is needed for the dollar to strengthen and stocks to rise in this depression, in spite of dollar strength, is a massive increase in the current rate of return on assets, which sees a return of capital back to the US. In the absence of rising financial leverage (unlikely due to the state of the banking sector) and with lower consumer spending guaranteed, this would require an almost impossible rise in productivity. Something akin to the dot.com boom cannot be entirely ruled out, however. 1%

2) Dollar Weakness & Equity Strength. This basically calls for a continuation of the current trend. Hyperinflation would certainly be consistent with this view, but it seems unlikely. What is slightly more likely is a steady decline in the dollar coupled with a continued rise in risk appetite backed up by improving US economic fundamentals, which all serve to prolong the current bubble. While this would not be sustainable, over a six month horizon it is certainly possible for it to continue. 12%

3) Dollar Weakness & Equity Weakness. This more realistic. The reasons to expect dollar weakness are all-too obvious, and while we have seen dollar weakness translate into equity strength in recent months this need not continue. In fact, as I write this post, the Dow is falling hard while the dollar is still weak (the Dow is getting KILLED in Aussie dollar terms, and the long-term downtrend is still in place). If emerging market demand for commodities remains strong and the Chinese revalue the yuan, commodities prices could rise substantially, squeezing companies’ top line growth and raising costs. While I don’t want to read to much into daily moves, I think it is significant that the Dow Transports rolled over today (not confirming the break-out according to Dow Theory) as oil spiked higher. While I would expect this trend to be short-lived, the period from H207 to H108 showed this relationship can go on for a long time.

4) Dollar Strength & Equity Weakness. This is my core view. True, I have held this view since Dow 9,000 and EUR1.4000/US$, but with the Dow now at 10,000 and the euro at EUR1.5000/US$, and the fundamentals unchanged, I like it even more. After all, the idea is to buy low and sell high is it not? I find it strange that people are jumping into the Dow now when they didn’t want any of it at 7,000, and are scrambling out of dollars when they couldn’t get enough of them at EUR1.3000/US$ a year ago.

Do you remember 12 months ago when the prevailing wisdom was that no matter what the government/Fed did to crush the dollar (and everyone new that’s what they were going to try and do), private sector deleveraging would ensure that the dollar continued to strengthen and asset prices continued to fall? If I had told you then that in less than a year’s time the Argentine Merval stock index would be pushing all-time highs, or that the AUD would be heading for parity against the dollar I’m pretty sure I would have been laughed at. Of course, I didn’t say those things. I was part of the consensus that thought the Fed could not overwhelm the natural deflationary pressures at play, and that the trend of deflation would continue. As far as I could see the Fed was just ‘pushing on a string’.

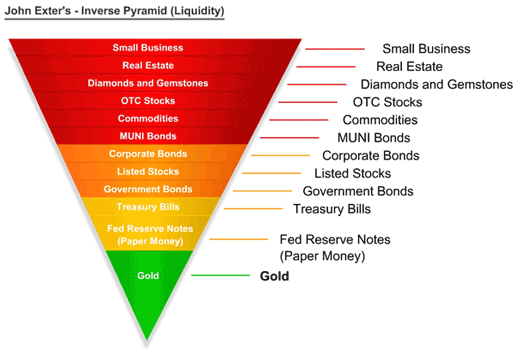

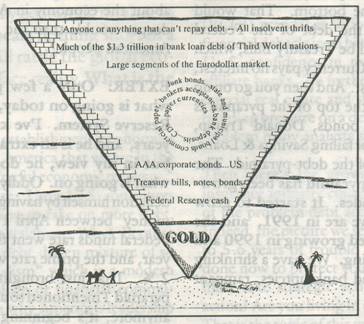

But my point is that the market works by exerting the maximum amount of pain on the maximum amount of people, and the thing that the fewest people expect is the thing that invariably happens. What if in 6 months time the DXY was back at the early-2009 highs? What if the Dow was below 6,500? What if the Fed indeed turned out to be impotent and a wave of private sector deleveraging overwhelmed their re-flation efforts? What if the rally since March turned out to have been driven by a temporary rise in optimism that was merely encouraged by the Fed? What if this has just been a bear-market rally within a longer-term debt-deflation spiral and the continued evaporation of the global debt pyramid?